Apr 29, 2021

Follow us on Google for more Moneywise news

Add us on GoogleFamilies are still a few months away from the monthly payments — stimulus checks, of a sort — that they're scheduled to get during the second half of this year. Yet President Joe Biden is already proposing to keep that cash flowing for at least a few more years.

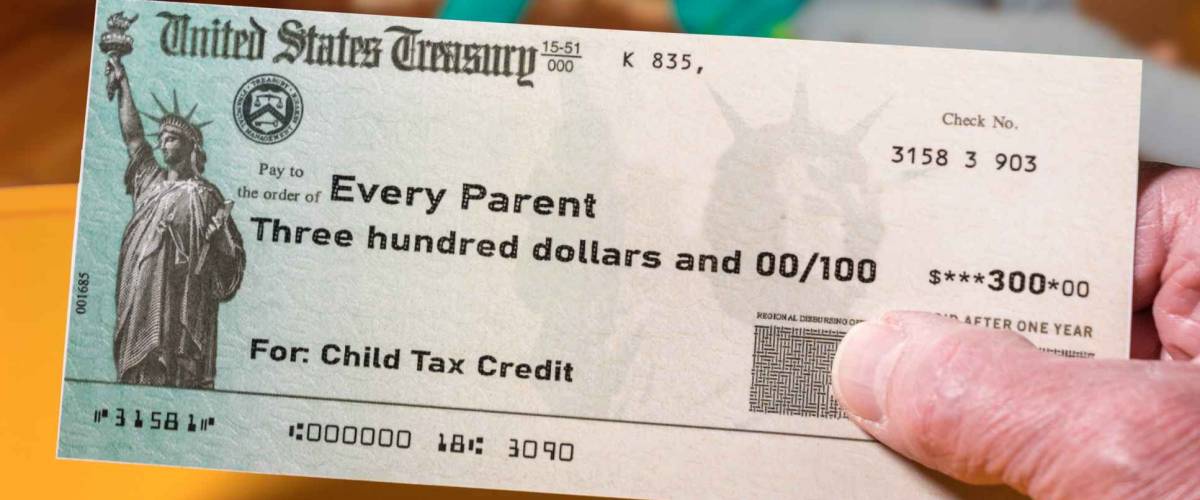

The checks, for up to $300 per child per month, are scheduled to start going out in July as part of a one-year expansion of the child tax credit. Biden would make the beefed-up credit a little less temporary under the "American Families Plan" he laid out in his big speech to Congress Wednesday night.

Advertisement

Some Democrats want to go even further and make the payments a permanent fixture, to help families pay essential bills and fight debt, and to reduce child poverty in the U.S.

Thanks for subscribing!

The money news that actually matters.

By signing up, you accept Moneywise Terms of Use, Subscription Agreement, and Privacy Policy.

Proposals would extend the new child tax credit

The child credit was expanded for 2021 through the massive COVID relief package Biden signed in mid-March. It's the bill that's been providing most Americans with the more conventional stimulus checks for up to $1,400 each.

Couples who file taxes jointly and earn less $150,000, and individuals who make under $75,000, get tax credits of $3,600 for each kid who's 5 or younger, and $3,000 per child ages 6 through 17.

"With two parents, two kids, that's up to $7,200 in your pocket to help take care of your family," Biden said during his speech. Households are getting up to $1,600 more per child than they did under the previous version of the credit.

Families will receive the first half of the fatter credit in the form of monthly checks of either $250 (per child 5 and under) or $300 (per child 6 to 17) starting in July and continuing through the end of the year. The remainder can be taken as a refund when you file your 2021 taxes next year.

Biden's families plan would continue the child credit expansion — and presumably the checks, too — through 2025.

Advertisement

But that's not enough for several Democrats in Congress, who are pushing to make the larger child credit permanent.

"For our economy to fully recover from this pandemic, we must finally acknowledge that workers have families, and caregiving responsibilities are real," says Rep. Richard Neal of Massachusetts, chairman of the tax-writing House Ways and Means Committee. He has introduced a bill to permanently extend the credit.

Must Read

- The ultra-rich use these 5 real estate strategies to build wealth while they sleep — you can start with just $100

- Here’s the average income of Americans by age in 2026. Are you keeping up or falling behind?

- Insurance companies profit most from drivers who auto-renew without shopping around. Comparing 100+ quotes takes 2 minutes and costs nothing

Join 250,000+ readers and get Moneywise’s best stories and exclusive interviews first — clear insights curated and delivered weekly. Subscribe now.

The costs may be a big obstacle

Republicans have bristled at the price tag for Biden's families package: $1.8 trillion.

More than $400 billion of that would come from extending the child credit for four years, based on an estimate from the congressional Joint Committee on Taxation that just one more year would cost around $109 billion.

Making the expansion permanent would cost taxpayers roughly $1.6 trillion, according to an analysis from the Tax Foundation.

Advertisement

Republicans and many of the country’s business leaders are alarmed by how Biden plans to pay for the child credit extension to 2025 and the rest of his families plan: with tax increases on the wealthiest Americans, including a hike in the top capital gains tax on millionaires to 39.6%.

"Even more taxing, even more spending to put Washington even more in the middle of your life from the cradle to college" is how South Carolina Sen. Tim Scott summed up the president's proposals Wednesday night in the Republican response to Biden's address.

Given the ultra-slim majority that Biden's party holds in the U.S. Senate, all Democrats would have to get behind the families bill in order for it to pass. And that's far from assured, considering the weight Wall Street money still carries with both major parties.

What if your family needs extra cash now?

If the bigger child tax credit is extended, your family could be provided with a significant amount of assistance for at least five years. But it's not clear whether Biden has a chance of getting his new plan across the finish line — and that first check in July may seem like a long way off if you’re feeling a cash crunch today.

Here are some options to cut costs and earn extra money to fill the gap:

-

Shave down the cost of your debt. If you’ve been relying on credit cards throughout the COVID crisis, the interest is bound to get expensive. A debt consolidation loan at lower interest can help you clear those balances more quickly and affordably.

-

Don't pay too much for insurance. Because people have been driving less and staying home more during the pandemic, some car insurance companies have doling out discounts. If yours won't give you a break, shop around for a better deal. You also might save on your homeowners insurance by comparing rates to find a lower price on that coverage.

-

Refinance your mortgage and slash your payments. If you own your home, mortgage rates are still at some of the lowest levels in history, and refinancing could save you thousands over the next year. Mortgage tech and data provider Black Knight recently said 13 million mortgage holders could cut their monthly payments by an average $283 through a refi.

-

Grow some money by investing spare change. You don't have to be rich to earn returns in the soaring stock market. A popular app helps you build a diversified portfolio just by investing "spare change" from everyday purchases.

You May Also Like

- JP Morgan sees gold hitting $6,000/oz before 2027 — and a Gold IRA lets you hold the physical metal while deferring the tax bill. Get your free guide from Priority Gold

- Dave Ramsey warns nearly 50% of Americans are making 1 big Social Security mistake — here’s what it is and the simple steps to fix it ASAP

- Thanks to Jeff Bezos, you can now become a landlord for as little as $100 — and no, you don't have to deal with tenants or fix freezers. Here's how

- Millionaires under 43 are reshaping investing — just 25% of their portfolios are in stocks. Here’s where their money is going

Clayton Jarvis is a mortgage reporter at MoneyWise. Prior to joining the MoneyWise team, Clay wrote for and edited a variety of real estate publications, including Canadian Real Estate Wealth, Real Estate Professional, Mortgage Broker News, Canadian Mortgage Professional, and Mortgage Professional America.

Mortgages • Mar 19

Mortgage applications are down as homeowners say ‘No thanks’ to refi savings

Banking • Mar 08