Apr 18, 2024

Some college students have enough financial help to focus on schoolwork and forging new friendships. Others are stressed about money all the time.

But regardless of your current means, financial literacy is an essential life skill for all young adults.

Advertisement

Some of the decisions you’re making now will affect the race you’ll be running for years to come — especially if student loan debt is putting you 10 feet behind the starting line.

Thanks for subscribing!

Take control — get our free newsletter.

By signing up, you accept Moneywise Terms of Use, Subscription Agreement, and Privacy Policy.

In the end, time is the only resource you can’t recover, and you can’t always make up for missed opportunities later. Here’s how to get up to speed.

What is financial literacy?

Financial literacy refers to a basic understanding of essential financial topics and skills. You don’t need to learn how to run a business; it’s about personal finance, the kind that grows and shrinks your own bank account.

Concepts that fall under the financial literacy umbrella include saving, learning how to build credit, investing, paying off debt, retirement planning and more.

Keep in mind, financial literacy doesn’t just consist of knowing all the definitions. It's also applying that knowledge in the real world through smart money management.

Once you have the tools, your long-term financial success won’t be based on hopes, dreams and guesswork. You’ll know what you need to do to achieve your financial goals.

Why is financial literacy important for students?

At first, financial literacy might seem like a game for older people — individuals who are far along in their careers and have more disposable income than the average college student.

In truth, financial literacy holds particular significance for college students given their constrained financial resources. As many students are living on their own for the first time, they immediately grapple with the reality of housing insecurities. A recent survey suggested that 55% of Los Angeles Community College District (LACCD) students experience housing insecurity while 19% are homeless.

Many students are living on their own for the first time but don’t have cash to burn on simple mistakes. That turns budgeting and financial planning into urgent priorities.

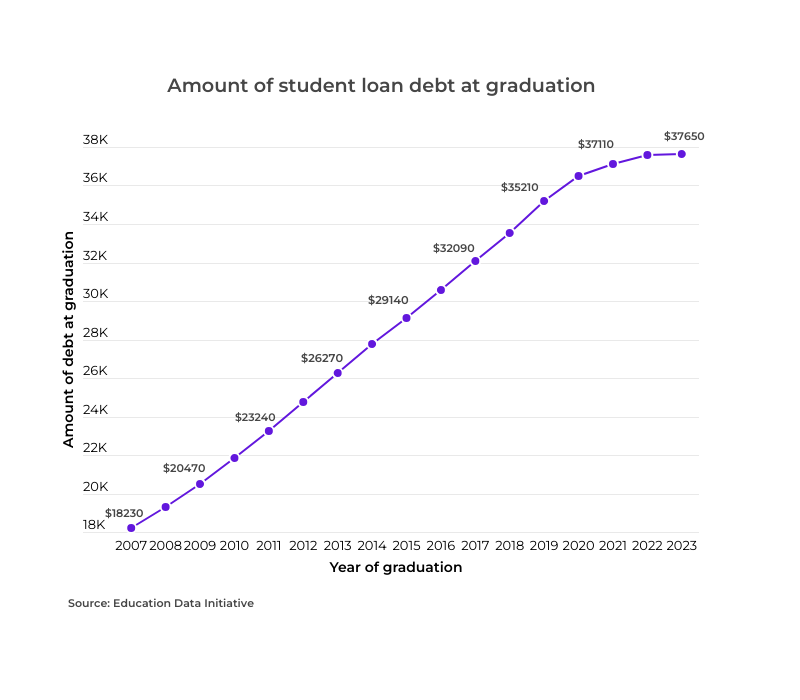

And it’s not like graduation brings immediate relief. Average student debt upon leaving school has skyrocketed to $37,650 — that’s up 322% since 1970, when adjusted for inflation.

A quarter of college students have experienced food insecurity, and 17% have experienced housing insecurity, a recent survey revealed

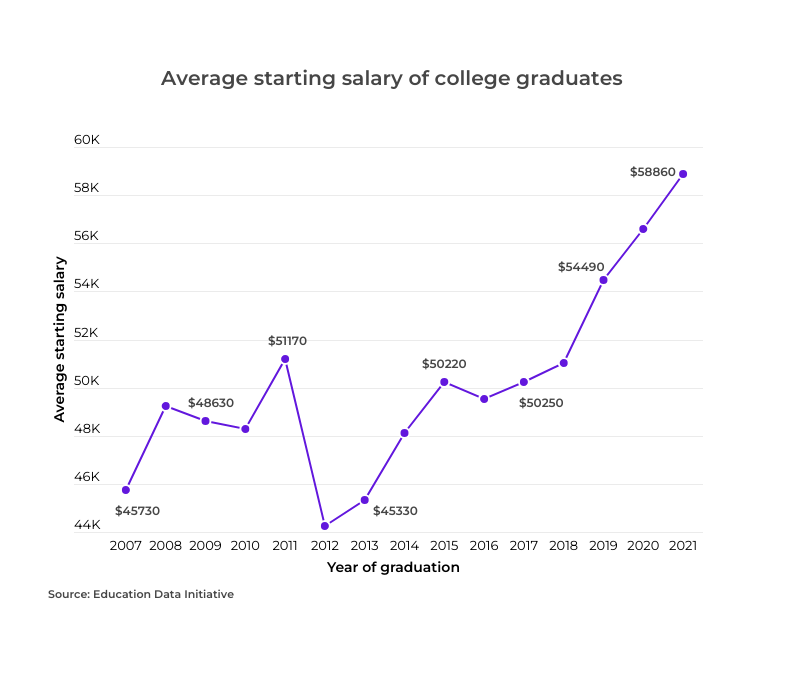

That looks like a lot of money for a recent grad — and it is — but you’ll be able to start mapping out a plan once you get an idea of your starting salary.

The average starting salary of bachelor’s degree holders over the past 10 years is $52,390. Obviously, a lot depends on your field. You can get a better idea of your individual prospects by searching for the job you want on the government’s Bureau of Labor Statistics website.

This will help you calculate your debt-to-income ratio, or DTI, which is a key budgeting and borrowing measurement.

To calculate your DTI, take your total monthly debt payments and divide the figure by your gross monthly income (how much money you earn each month before taxes and deductions are subtracted).

The DTI for the class of 2021 is around 63% — not as bad as the class of 2018 at 66%, but still a high DTI.

Advertisement

Lenders typically want to see this percentage much lower when it comes to approving loans, especially big ones like mortgages and auto loans, because it signals a higher likelihood of repayment.

A DTI of less than 43% shows you can handle your debts and will make it easier to get a reasonable loan.

Must Read

- The ultra-rich use these 5 real estate strategies to build wealth while they sleep — you can start with just $100

- Here’s the average income of Americans by age in 2026. Are you keeping up or falling behind?

- Insurance companies profit most from drivers who auto-renew without shopping around. Comparing 100+ quotes takes 2 minutes and costs nothing

Join 250,000+ readers and get Moneywise’s best stories and exclusive interviews first — clear insights curated and delivered weekly. Subscribe now.

5 pillars of financial literacy

Financial literacy covers a wide range of topics, but they can be sorted into five key categories.

Here’s a quick look at each one, touching on some of the most important elements you’ll want to learn about:

Earn

It’s not enough to know how much you make; you need to understand what happens to the money.

Say you apply for a summer job. Your employer will quote you a pre-tax salary, often through a written work contract. You’ll want to do the math to determine what that number will look like after federal taxes as well as other deductions including states taxes and Social Security contributions.

This will give you an accurate expectation of your net or take-home pay so you can budget accordingly.

Spend

Some spending is essential: You need to eat, get around, pay for school and keep a roof over your head. Some spending is not.

Your job is to correctly identify which is which, and to stay on budget while minimizing your costs and maximizing the value you get back.

Start by tracking your spending, either manually or with an app that watches your bank account. You can only make a decision about whether $150 a month is too much to spend on takeout if you know you’re spending $150 a month.

Then, take the time to really research your options. A lot of similar products and services are sold for wildly different prices — including food, clothes and insurance — and you should only spend extra when it makes you happier.

Save and invest

Many college students treat this as a problem for “later,” but you’d be surprised how quickly “later” can arrive. Saving and investing are not voluntary but critical to long-term financial stability and achieving your life goals.

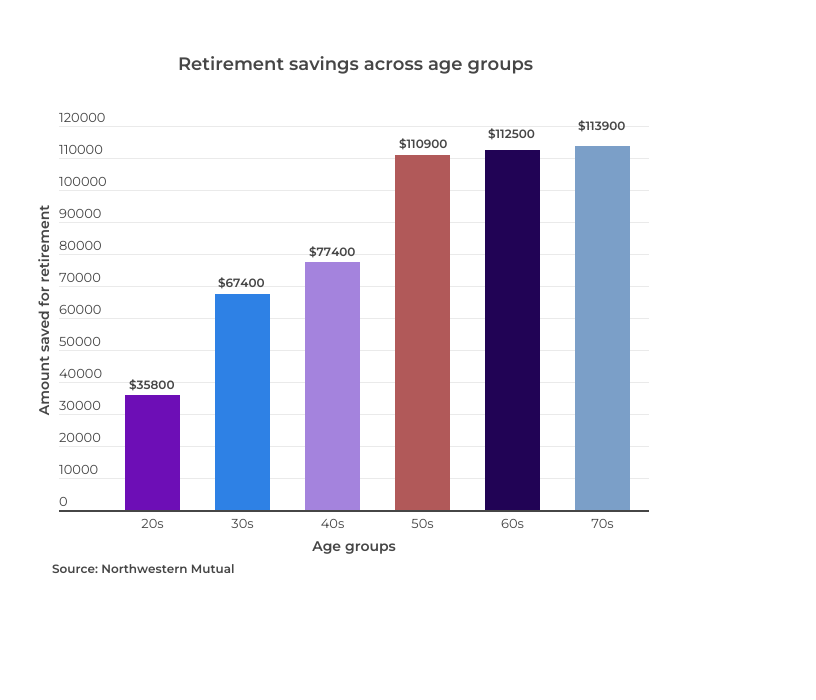

The main goal now is to make saving and investing a consistent habit as you grow your earnings over time. A recent study by Northwestern Mutual shows how different age groups have saved up for their retirement — the average savings of U.S. adults rose by 3% in 2023, reaching $89,300 from $86,869 in 2022.

Advertisement

Plus, due to compounding, the saving and investing you do now is worth a lot more than the saving and investing you’ll do later.

Compounding happens when the interest you make in a savings account begins generating its own interest, or the earnings you make on your investments get reinvested and begin generating their own earnings.

This effect can ramp up quickly, even with a small amount of money. It’s starting early that’s the key.

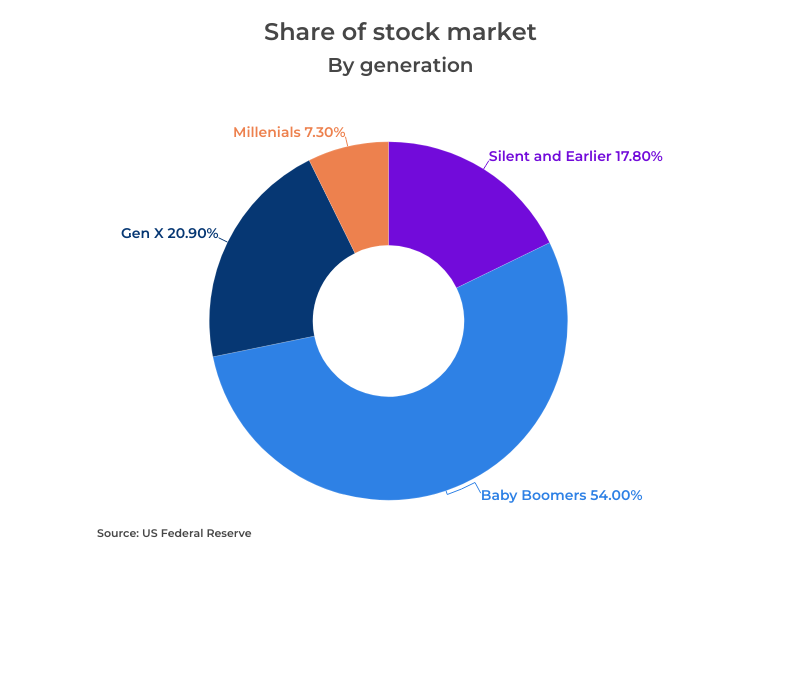

Millennials don’t own a very big slice of the stock market, data from the Federal Reserve shows, but don’t let that stop you from learning about different kinds of investments and putting any spare cash you have to work.

Borrow

Even if you’ve managed to pay for college without taking out huge student loans, you’ll likely borrow lots of money in lots of different ways throughout your life.

That includes mortgages for buying a home, auto loans for financing a car and credit cards for day-to-day purchases. Understanding how these loans work and what options are available will help you avoid major pitfalls.

Credit cards, for instance, offer convenience due to their widespread acceptance and ease of use, although they may come with higher costs compared to alternative borrowing options. Some loans are secured, which are cheaper but you must agree to surrender something of value if you stop paying. Some loans are closed, meaning you can’t simply pay them off quickly if you want to.

Take the time to determine the best kind of loan for your situation, then compare offers from different lenders. Pay close attention to the interest rate and how long you have to pay the loan back, and watch out for fees hidden in the fine print.

Protect

Making money isn’t easy, so don’t lose it to a catastrophe you weren’t prepared for.

Protecting yourself starts with an emergency fund — a set amount of cash you leave aside in your bank account for unexpected financial needs. That way, when your laptop gets stolen, you don’t need to borrow money (and thus spend more) to pay for it.

The other big element is insurance. Car insurance, renter’s insurance and health insurance will all drain your finances, but you’ll be glad you have them when you need them.

The key is picking the right kind and amount of coverage — so you’re not overprotected and overspending, or underprotected and underspending — and comparing offers from several providers. Different companies use different formulas to determine their rates, so you can save a lot just by shopping around.

11 statistics on financial literacy

Don't feel like a star student when it comes to financial literacy? The truth is that many Americans are lacking in this area, which can have a cascade of consequences for their financial well-being.

Take a look at these 11 statistics — and be inspired to do better than your classmates and neighbors.

-

Americans rank 14th in financial literacy globally.

-

Nearly 43% of Americans failed a National Financial Literacy Test.

-

The average score on the National Financial Literacy Test among people aged 19 to 24 is 64%.

-

70% of U.S. adults feel financial anxiety, and 52% say their financial stress has increased since before the pandemic.

-

In the past three months, 43% of women have reported an increase in concerns about their financial situation, which is 8% higher than the corresponding figure for men.

-

27% of millennials are doing better than their parents were at their age.

-

Approximately 19% of Gen X lack confidence in their ability to retire before reaching 80, and 11% believe that they may never retire.

-

About 27% of millennials have reported not being aware of their credit score.

-

Only 39% of college students answered over half of the five multiple-choice questions correctly, which covered topics like credit scores, loans, retirement savings, investing, and interest accrual.

-

88% of Americans said that high school did not adequately prepare them for managing finances in real-life situations.

-

Currently, 35 states in the United States have made it a requirement for students to complete a personal finance course as part of their graduation.

Advertisement

5 places to go to improve your financial literacy

Unless you’re born rich, you won’t be able to reach financial security without working on your financial literacy.

Now, if you haven't had any financial education until now — and that describes plenty of young people — you may not know where to turn.

There isn’t one right answer, so here are just a few of your options to get the financial knowledge you need.

Take finance courses at college

You're a student, so make the most of this time. If your college or university offers financial literacy courses, seize the opportunity to learn in a structured setting and maybe earn a couple credits.

If personal finance courses aren’t available, even something as broad as economics can prove useful in learning about topics such as inflation, stock market crashes and housing bubbles — all things that can have a very real impact on your life now and in the future.

Leverage government and nonprofit resources

While education is primarily a state and local responsibility, there are some federal resources available to all Americans.

The U.S. government has set up various platforms to help people learn about personal finance and get specific questions answered. MyMoney.gov, run by the U.S. Treasury's Financial Literacy and Education Commission, is a great starting point.

Other agencies include the Consumer Financial Protection Bureau, the U.S. Securities and Exchange Commission and the Internal Revenue Service.

Nonprofits are another option. For example, United Way sometimes offers free financial coaching.

Turn to financial institutions and experts

Banks and credit unions provide a wealth of financial information to customers and the general public. Check your bank’s website to see which services it has to help you, from article libraries to budgeting tools and calculators.

You can also consult financial professionals, either through your bank or independently, to help with tasks like setting up investment accounts.

Keep in mind: Not all advice is free, and not all advice is unbiased, so ask a lot of questions and compare with other resources before accepting what you hear.

Consider less traditional resources

Not everybody has the time or patience to take a class or poke around on government sites. Sometimes you want information to reach you where you are.

While social media is a swamp of bad advice, you can find people who really know their stuff.

Just do your due diligence when consulting online sources, and always look at a person's qualifications and background. Being on social media doesn’t mean someone is impartial, and having a lot of followers doesn’t mean they’re giving good advice.

Follow personal finance sites

Moneywise isn’t your only option, of course, but we try to provide easy access to tools and resources to help you master essential money matters.

We’re not know-it-alls — in fact, we try hard not to become know-it-alls. We’re always curious and always learning, and we like to take our readers along for the ride as we discover new ways to get the most from your money.

If you’re looking for well-researched articles that won’t make your eyes glaze over, head over to Moneywise or sign up for our email newsletter.

You May Also Like

- JP Morgan sees gold hitting $6,000/oz before 2027 — and a Gold IRA lets you hold the physical metal while deferring the tax bill. Get your free guide from Priority Gold

- Dave Ramsey warns nearly 50% of Americans are making 1 big Social Security mistake — here’s what it is and the simple steps to fix it ASAP

- Thanks to Jeff Bezos, you can now become a landlord for as little as $100 — and no, you don't have to deal with tenants or fix freezers. Here's how

- Millionaires under 43 are reshaping investing — just 25% of their portfolios are in stocks. Here’s where their money is going

Kevin Hamilton is the senior editor of Moneywise.com. An award-winning graduate of Toronto Metropolitan University’s school of journalism, Kevin made his mark at a number of publications including Metro, the Toronto Star, Huffington Post and Toronto Life.

Managing Money • Jun 08

How to check your credit score for free

Banking • May 12