Jun 16, 2023

After years of covering personal finance advice, there’s one simple money fact that keeps spilling into every financial decision I make:

Every $1 you save by 35 becomes at least $10 by 65

The news is even better if you’re young. Every $1 saved by 25 becomes $20 by retirement. All you need is a retirement account generating the usual 8% returns and compound interest will take care of the rest.

Thanks for subscribing!

Invest smarter with our free newsletter.

By signing up, you accept Moneywise Terms of Use, Subscription Agreement, and Privacy Policy.

So what is compound interest? Why do wealth advisors talk about it like it’s the greatest thing since sliced bread? Most importantly, how can it grow even the smallest, most conservative investment portfolio into a sizable fortune?

The short version

- Compound interest is interest paid on the principal plus any interest already accrued.

- The use of compound interest is one of the main benefits of investing.

- You can calculate how much your investments could earn from compound interest using the Rule of 72.

Must Read

- The ultra-rich use these 5 real estate strategies to build wealth while they sleep — you can start with just $100

- Here’s the average income of Americans by age in 2026. Are you keeping up or falling behind?

- Insurance companies profit most from drivers who auto-renew without shopping around. Comparing 100+ quotes takes 2 minutes and costs nothing

Join 250,000+ readers and get Moneywise’s best stories and exclusive interviews first — clear insights curated and delivered weekly. Subscribe now.

What is compound interest?

To illustrate the potential of compound interest, let’s start at the beginning. How does interest work and why is compound interest the most powerful kind?

What is interest?

In its simplest form, interest is the fee charged for money borrowed. Interest can work for or against you.

If you’re the investor/lender, e.g. you loan money to your bank via a CD, you’ll be earning interest on your investment as a bonus for lending your money.

On the flip side, if you’re the borrower, e.g. you take out a mortgage, you’ll be paying interest as a fee for the service of borrowing money. The same goes for your credit card debt, where a high annual percentage rate (APR) can spiral into exponential debt and negatively impact your credit score.

Although the interest rate is essentially the “price” of the loan, you’ll almost never see it listed by itself on a loan document when you borrow money. Instead, it’ll be bundled together with most/all of your additional lending fees into a single percentage called the APR.

Now, when you’re earning interest, your gains are expressed as an annual percentage yield*,* or APY. That’s why you’ll always see CDs and savings accounts ranked by their APY; higher is better.

In short, interest is the fee for borrowing money. The interest rate is expressed as APR when you pay it and APY when you earn it.

What is compound interest?

As we’ll see in the calculations below, the amount of interest that accrues on a loan is heavily dependent on the principal*,* or loan amount.

- Simple interest is based on the principal

- Compound interest is based on the principal plus interest already accrued

Simple interest is static and linear, while compound interest is dynamic and exponential. We’ll play with a compound interest calculator below, but first, let’s dive into examples of each.

Compound interest vs. simple interest

Let’s say you invest $100,000 into two accounts for five years.

- Account 1 generates 10% simple interest

- Account 2 generates 10% interest compounded annually

Calculating the interest you’ll earn from Account 1 is pretty straightforward. You’ll generate 10% of your initial principal capital each year for five years, so that’s $10,000 x 5 = $50,000 in total interest. Not bad.

But Account 2 generates compound interest, meaning your interest earns interest, too. Each year, you’ll earn 10% of what’s currently in the account, not just the principal.

- After year 1, you’ll earn 10% of $100,000 = $10,000

- After year 2, you’ll earn 10% of $110,000 = $11,000

- And after year 3, you’ll earn 10% of $121,000 = $12,100

And so on. In total, after five years:

- Account 1 is worth $150,000

- Account 2 is worth $161,051

By simply compounding your interest annually, you earned $11,051 extra on your investment than you would via simple interest — that’s 11% of your initial investment!

And since simple interest is linear and compound interest is exponential, the gap will grow even wider after time.

In 15 years,

- Account 1 will be worth $250,000.00

- Account 2 will be worth $417,724.82

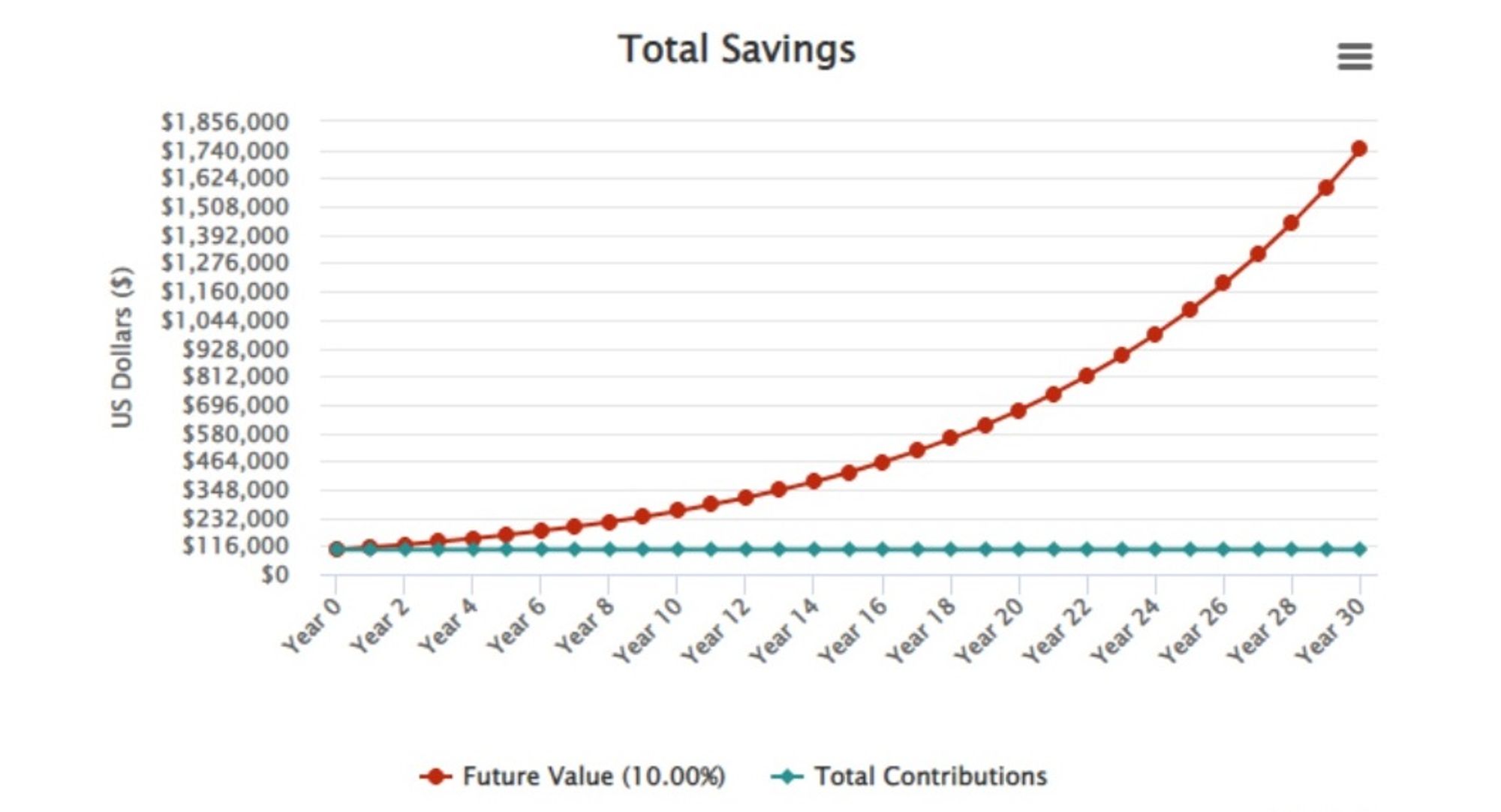

In 30 years,

- Account 1 will be worth $400,000.00

- Account 2 will be worth $1,744,940.23

Courtesy of Investor.gov

How does compounding frequency affect overall ROI?

You might be wondering: how much would your investment be worth if the interest was compounded more frequently than once a year? What about monthly, daily or even continuously compounding interest?

Compounding more frequently does increase returns, but perhaps not quite as much as you’d think.

Here’s how shaking up the compounding frequency would affect Account 2’s value over 15 years:

| Compound frequency | Value of $100,000 investment after 15 years at 10% | Delta from previous compounding frequency |

|---|---|---|

| Annually | $417,724.82 | – |

| Semi-annually | $432,194.24 | $14,469.42 |

| Monthly | $445,391.96 | $13,197.72 |

| Daily | $448,076.84 | $2,684.88 |

| Continuously | $448,168.91 | $92.87 |

There’s a nice leap from annually to semi-annually compounding interest, and then again from semi-annually to monthly. Once you go more frequently than that, there’s a steep drop off.

Moral of the story? Don’t be seduced by investments offering continuously compounding interest — it’s mostly marketing fluff.

But compound interest itself is far, far from fluff.

How does compound interest work for investors?

Interest makes your money grow. Compound interest makes your money grow faster.

When you earn interest on your interest, you strap your savings to an exponential growth curve that takes off like a rocket.

But let’s support that hyperbole with some numbers. Now would be a good time to introduce you to the Rule of 72, which can help give you a quick, general estimate for how quickly an investment with compounding interest can take off.

The Rule of 72 states that if you take the number 72 and divide it by your compound interest rate, it’ll give you a rough idea of how many years it’ll take to double.

So, for example, if you invest $100,000 in a retirement account with ~8% APY, it’ll take:

- 72 / 8% APY = 9 years to become roughly $200,000

The Rule of 72 is only really accurate for interest rates between 5 and 10%. For rates outside of that range, consider using the Rule of 69.3 — which is more accurate but requires a calculator.

I like the Rule of 72 because it puts the power of compound interest into context. 8% APY may not sound like a lot, but when you realize it doubles your money in just 9 years, it’s much more appealing.

More: How to invest money wisely

How does compound interest work with the stock market?

You probably noticed that I started this piece talking about loans and borrowers, but the last section referenced a retirement account, which is a stocks/bonds investment.

Do stocks generate interest, too?

Not in the formal sense. Stocks are not loans; they’re literal part ownership of a company. There’s no predetermined interest rate for 100 shares of AAPL like there is with a savings account.

So no; stocks do not generate compound interest — but they do have compounding value.

Let’s say you invest $100,000 in an S&P 500 index fund with an average annual return of 9% and very little variance. Next year, your shares will be worth $109,000. The year after that, they’ll be worth $109,000 x 1.09 = $118,810. The year after that, $129,509.29.

Therefore, while 9% is not an interest rate in the technical sense, your stock market investment is still compounding in value. Therefore, the principles of compound interest can be applied to long-term stock market investments, as well.

But as you’re tinkering with your own financial calculators, don’t forget to factor in the key difference between a savings account with a fixed interest rate and a stock market investment. The latter involves some risk, and isn’t always guaranteed to produce regular returns (or positive returns at all!).

How to calculate compound interest

Here’s the actual compound interest formula:

So let’s calculate how much an investment of $50,000 compounded monthly for 14 years at 7.6% APY would generate:

I = $50,000(1 + 0.076/12)12 x 14 – $50,000 = $94,411.64

Remember, this formula calculates interest earned. You can calculate the current value of the account by not subtracting the second P.

The bottom line

Compound interest is how half of rich Americans got rich. They didn’t have to earn a high salary, buy Bitcoin in 2012, or even day trade; they simply poured money into savings and conservative investment portfolios and let compound interest do the rest of the work.

When your interest earns interest, and that interest earns interest, your wealth starts accumulating exponentially. Therefore, the future value of $1 saved at 35 becomes $10 by 65.

That’s a lot — and all the more reason to start earlier.

You May Also Like

- JP Morgan sees gold hitting $6,000/oz before 2027 — and a Gold IRA lets you hold the physical metal while deferring the tax bill. Get your free guide from Priority Gold

- Dave Ramsey warns nearly 50% of Americans are making 1 big Social Security mistake — here’s what it is and the simple steps to fix it ASAP

- Thanks to Jeff Bezos, you can now become a landlord for as little as $100 — and no, you don't have to deal with tenants or fix freezers. Here's how

- Millionaires under 43 are reshaping investing — just 25% of their portfolios are in stocks. Here’s where their money is going

Miranda Marquit is a journalism-trained freelance writer and professional blogger specializing in personal finance.

Managing Money • Nov 01

How to get started using Quicken

Investing • Jan 02