Mar 25, 2021

Your credit score is very important for many different financial goals, but you can't have good credit without first establishing your credit history.

There’s more to your credit score than how much you owe. The age of your accounts is a factor too — and an important one.

Advertisement

The further back your credit history goes, particularly if it’s a good credit history, the better it is for your overall score and your borrowing options.

Thanks for subscribing!

Take control — get our free newsletter.

By signing up, you accept Moneywise Terms of Use, Subscription Agreement, and Privacy Policy.

Here are some quick facts about credit history and different ways to boost your score:

The starting point

In order to start building a credit score, you must have an account that reports your payment history and balance to one of the three big credit bureaus: TransUnion, Experian and Equifax.

You need at least six months of credit history to qualify for a FICO credit score — which is the most common scoring metric. Your credit history makes up 15% of your FICO score.

Six months is pretty much the bare minimum in terms of credit history. In many cases, lenders consider anything between two to four years of history a good starting point. A solid history that will count as a positive in your favor is about 10 years of good credit.

Must Read

- The ultra-rich use these 5 real estate strategies to build wealth while they sleep — you can start with just $100

- Here’s the average income of Americans by age in 2026. Are you keeping up or falling behind?

- Insurance companies profit most from drivers who auto-renew without shopping around. Comparing 100+ quotes takes 2 minutes and costs nothing

Join 250,000+ readers and get Moneywise’s best stories and exclusive interviews first — clear insights curated and delivered weekly. Subscribe now.

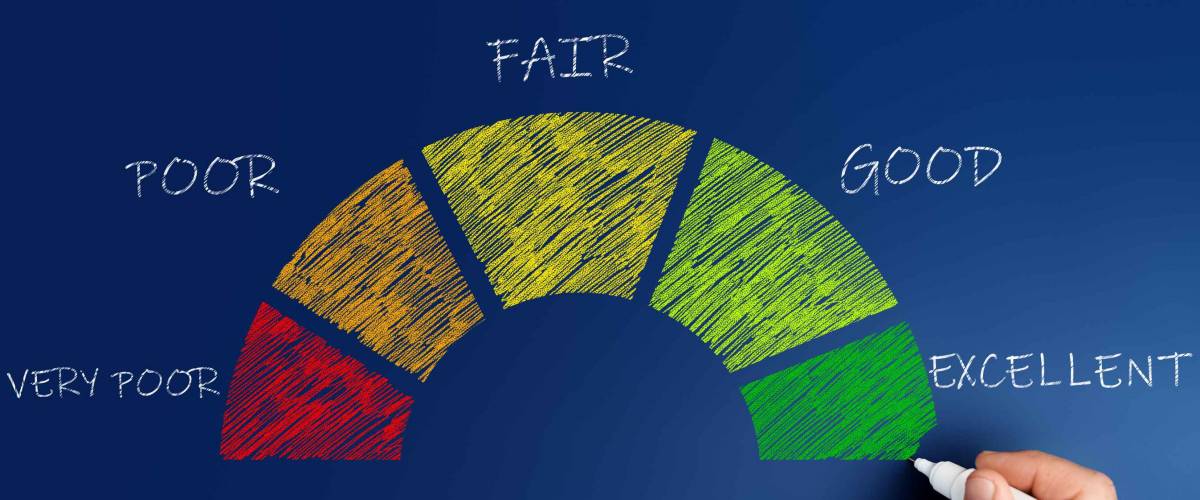

What is a good credit score?

Credit scores from 580 to 669 are typically considered fair. A score of 670 to 739 is considered good; 740 to 799 is seen as very good; and 800 and higher is considered excellent. If you’re just starting out building your credit, a score in the low 700s is a good target to aim for.

Advertisement

When you begin building credit, however, you don’t start with a 0 or a very low number like 300.

Precisely how credit is scored is the stuff of complicated algorithms and trade secrets, but there are things we know help it go up: pay your bills on time, don’t carry a big balance and don’t open too many accounts too close together.

With that said, here are some other ways to build your credit score.

Looking to keep building up your credit and get some rewards at the same time? You can get a no-fee, cash-back Visa card to do exactly that.

How time affects your credit score

Having older credit accounts with a good payment history shows lenders that you’re responsible with your financial obligations. But lenders will also look at other things, like the number of accounts you have and their average age.

Advertisement

Your overall credit history is tied pretty closely to the things you’d expect: Payment history, the amount of debt you’re carrying and new accounts you’ve opened recently. There are many factors that go into calculating your credit score, but hanging on to an older credit card you still use and shows a strong payment history is a good idea.

The other aspect to consider is the average age of your accounts. This is determined by just adding the age of each account and dividing it by the number of accounts.

Let’s say you have four credit cards: one is 12 years old, one is 7 years old, one is 4 years old and the newest is one year old. If you add up those ages (12 + 7 + 4 + 1 = 24) and divide that by the number of cards (four) you get an average account age of six years.

As you can see, every new credit card or account you add will lower the average age. And a slew of new accounts will lower it very quickly. And as far as lenders are concerned, the older the age the better, so it’s a great reason to steer clear of opening new cards too often.

Building a good score

Advertisement

One of the most important places to start when it comes to building and maintaining good credit is simply knowing what your credit score is.

There are sites that offer free credit monitoring, which is a great place to start getting into the habit of keeping an eye on it.

Maintaining a good credit history by keeping your balances low and making your monthly payments consistently. As you create a good payment track record, your credit score will gradually rise.

If you’re concerned that your credit score could use a bump in the right direction, there are also services designed to help you raise your FICO score.

And if your existing debt has you starting to feel swamped, [you should consider folding all of your debt into a consolidation loan with a lower interest rate.

- Credit building: If you need to build your credit up, there are dedicated credit-building services designed to help you do just that.

- Get a credit card designed to help you build your score: Provided you haven’t just just applied for or got a new credit card, you can sign up for a new card and get a jump on building your credit while enjoying benefits like no fees and cash back.

- Credit repair: Is your credit not where it should be and you need to put in the work to repair it? You can get a special credit-repair loan to help get your score back up.

You May Also Like

- JP Morgan sees gold hitting $6,000/oz before 2027 — and a Gold IRA lets you hold the physical metal while deferring the tax bill. Get your free guide from Priority Gold

- Dave Ramsey warns nearly 50% of Americans are making 1 big Social Security mistake — here’s what it is and the simple steps to fix it ASAP

- Thanks to Jeff Bezos, you can now become a landlord for as little as $100 — and no, you don't have to deal with tenants or fix freezers. Here's how

- Millionaires under 43 are reshaping investing — just 25% of their portfolios are in stocks. Here’s where their money is going

Justin Anderson was formerly a reporter at MoneyWise. He has a degree in Journalism from Ryerson University and his career has seen him cover everything from business and finance to the entertainment industry to politics, with plenty in between.

News • May 05

What is Dr. Anthony Fauci's net worth?

Insurance • Apr 20