Sep 19, 2025

The cost of borrowing has decreased after the September 17 rate announcement, as the Federal Open Market Committee (FOMC) reduced interest rates to a federal funds rate range of 4.00% to 4.25%.

This means the rates on credit cards and other variable-rate loans, including home equity lines of credit (HELOCs) will decrease.

Advertisement

What does the federal funds rate have to do with your debt? Here's a look at what the federal funds rate is and what it means for your loans.

Thanks for subscribing!

The money news that actually matters.

By signing up, you accept Moneywise Terms of Use, Subscription Agreement, and Privacy Policy.

What is the federal funds rate?

The federal funds rate is the target interest rate range that banks charge one another for borrowing money. The rate then affects consumers because it will also impact the interest rates they pay on loans, such as car loans, HELOCs and other debt like credit card rates.

The Fed officials announced on September 17 they are decrasing rates this month, bringing the target range to 4.00% to 4.25%.

Today’s rates are a big departure from just a few years ago. Back in March 2020, the federal funds rate sat at near zero, and in June 2021 policymakers predicted there would be no rate hikes in 2022.

However, the Fed increased the federal funds rate 11 times in an effort to combat inflation and slowly lowered rates to the range of 4.25% to 4.50% before deciding to hold rates steady for most of this year. The September 17 announcement is the first interest rate reduction since March.

Must Read

- The ultra-rich use these 5 real estate strategies to build wealth while they sleep — you can start with just $100

- Here’s the average income of Americans by age in 2026. Are you keeping up or falling behind?

- Insurance companies profit most from drivers who auto-renew without shopping around. Comparing 100+ quotes takes 2 minutes and costs nothing

Join 250,000+ readers and get Moneywise’s best stories and exclusive interviews first — clear insights curated and delivered weekly. Subscribe now.

Understanding the federal funds rate

The federal funds rate is dictated by Federal Reserve officials, specifically a 12-person committee — called the Federal Open Market Committee (FOMC) — that includes the chair of the Reserve, Jerome H. Powell. The FOMC meets eight times a year to discuss the rate, using indicators such as inflation to determine whether a hike is necessary.

Advertisement

The Fed interest rate hikes, or funds rate hikes, were meant to limit consumer demand. When the rate increases it indirectly affects the interest that consumers pay for loans, such as those used to buy a car or buy a house. The September 17 rate announcement suggests a balancing of risks.

In a statement, the Fed said "The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. Uncertainty about the economic outlook remains elevated. The Committee is attentive to the risks to both sides of its dual mandate and judges that downside risks to employment have risen."

"In support of its goals and in light of the shift in the balance of risks, the Committee decided to lower the target range for the federal funds rate by 1/4 percentage point to 4 to 4‑1/4 percent. In considering additional adjustments to the target range for the federal funds rate, the Committee will carefully assess incoming data, the evolving outlook, and the balance of risks."

How the federal funds rate impacts borrowing

Mortgages

The federal funds rate helps dictate the prime rate and variable mortgage rates, though not the rates on fixed home loans. Even so, new fixed-rate loans have been getting more and more expensive.

During the earlier stages of the pandemic, the Fed kept fixed mortgage rates in check by buying billions worth of Treasury bonds and mortgage-backed securities every month. Those purchases helped "foster smooth market functioning and accommodative financial conditions, thereby supporting the flow of credit to households and businesses," the central bank said.

But in May 2022, the Fed announced plans to begin selling off some of those assets.

Advertisement

The federal funds rate more directly affects other forms of borrowing, such as credit cards and car loans.

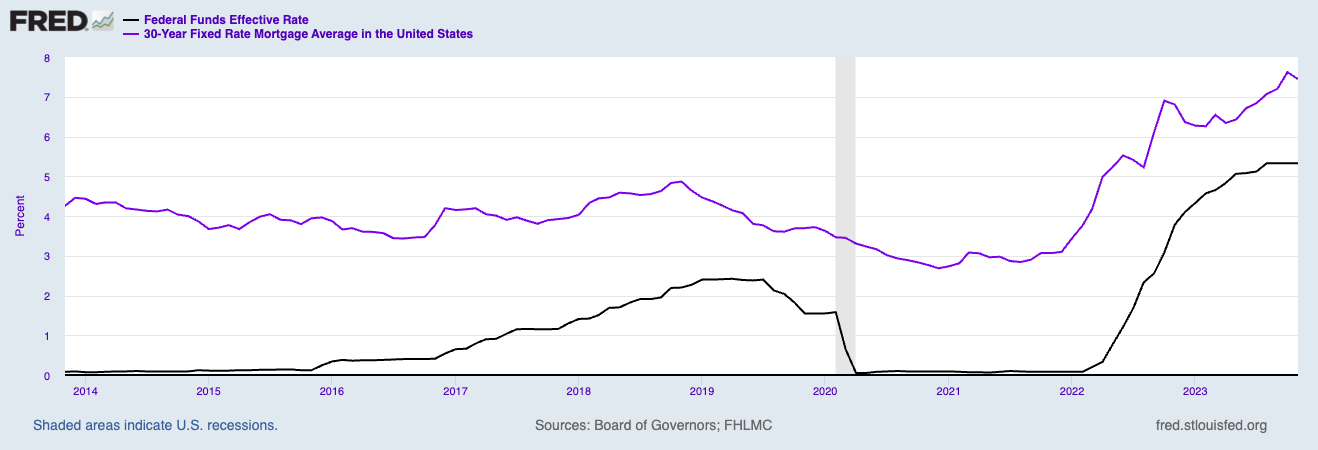

The federal funds rate and avg 30-year mtg rate, last 10 years

Credit cards

The interest rate hike also affects the interest you pay for credit card loans. The annual percentage rate (APR) determines how much you pay for any debt that is outstanding at the end of the month. The average APR has increased from 16% prior to 2022's first hike to 25.33% as September 19, 2025.

What does this mean for your credit card payments? Someone with a $15,000 credit card balance will now pay over $700 more in interest (compared to an APR of 16%).

Car loans

In the last quarter of 2022, the national average rate for a 60-month new car loan was 5.50% but that has increased with each rate hike. The average 60-month car loan rate sits at 7.67% as of May 2025, according to the Federal Reserve latest data.

However, keep in mind that factors such as credit score and vehicle type will affect your given rate.

HELOCs

Home equity lines of credit are also tied to the federal funds rate, although there is a less direct link. The interest rate for a HELOC is determined by the prime rate, which is usually 3% higher than the federal funds rate. Since HELOC lenders tie their rates to the prime rate, users with a variable rate HELOC will see their interest payments go up or down based on the federal funds rate.

When the federal funds rate increases, HELOC interest typically increases by the same amount. For a 10-year $30,000 HELOC, the average rate is 8.05% as of September 2025.

You May Also Like

- JP Morgan sees gold hitting $6,000/oz before 2027 — and a Gold IRA lets you hold the physical metal while deferring the tax bill. Get your free guide from Priority Gold

- Dave Ramsey warns nearly 50% of Americans are making 1 big Social Security mistake — here’s what it is and the simple steps to fix it ASAP

- Thanks to Jeff Bezos, you can now become a landlord for as little as $100 — and no, you don't have to deal with tenants or fix freezers. Here's how

- Millionaires under 43 are reshaping investing — just 25% of their portfolios are in stocks. Here’s where their money is going

Leslie Kennedy served as an editor at Thomson Reuters and for Star Media Group, followed by a decade in marketing communications, before returning to her editorial roots. She is a graduate of Humber College’s post-graduate journalism program and has been a professional writer and editor ever since.

Mortgages • Feb 19

Mortgage rate trends: Mortgage rates continue to decline

Banking • Nov 21