Dec 11, 2023

Follow us on Google for more Moneywise news

Add us on GoogleThe best gifts in life are unique, valuable, and memorable. And if you ask me, savings bonds check all three boxes.

By gifting a recent grad, infant nephew, or newlyweds some savings bonds, you’re giving them both a valuable asset and an invaluable learning opportunity since bonds are some of the most underrated, overlooked assets in the market.

But how do you gift savings bonds? Where do you buy bonds? And what types of savings bonds make for the best gifts?

Thanks for subscribing!

Invest smarter with our free newsletter.

By signing up, you accept Moneywise Terms of Use, Subscription Agreement, and Privacy Policy.

Why savings bonds make a great gift

What makes government-issue bonds such underrated gift ideas?

They’re memorable and unique

Amazon gift cards and Bluetooth speakers are great and all, but you’re bound to be the only one giving this person a government-issue bond. Even if they don’t appreciate it in the moment, they’ll surely remember it.

They’re learning opportunities

Children, students, and even some adults may never consider buying bonds until somebody purchases bonds for them. At that point, they’re more likely to take an interest in something they already have.

Later in life, simply knowing that I bonds exist can help them hedge their savings against inflation.

More: 10 gift ideas that teach kids about money

It’s the gift that keeps on giving

At the time of this writing, I bond rates are at 5.27%. EE bonds double in value after 20 years. So, in essence, you’re gifting someone a high-interest rainy-day fund or future student loan relief.

Must Read

- The ultra-rich use these 5 real estate strategies to build wealth while they sleep — you can start with just $100

- Here’s the average income of Americans by age in 2026. Are you keeping up or falling behind?

- Insurance companies profit most from drivers who auto-renew without shopping around. Comparing 100+ quotes takes 2 minutes and costs nothing

Join 250,000+ readers and get Moneywise’s best stories and exclusive interviews first — clear insights curated and delivered weekly. Subscribe now.

Which savings bonds can you buy as gifts?

For now, you can only issue two types of savings bonds as gifts: Series EE and Series I savings bonds.

EE bonds and I bonds have many similiarities:

- They’re locked up for the first year and mature after 30 years

- Cashing in between years one and five will forfeit three months of interest

- Interest is earned monthly and compounded semi-annually

- Both have a maximum annual purchase amount of $10,000 (although I bonds let you buy another $5,000 with your tax return), and

- Both are exempt from state and municipal taxes. They can also be exempt from federal taxes if used to cover qualified education expenses.

But here’s where things differ and why you may want to choose one type of bond over the other as a gift.

Series EE savings bonds

Series EE savings bonds, or EE bonds for short, have a fixed interest rate for the first 20 years that you or the gift recipient holds the bond. You’ll see this interest rate upfront.

At the time of this writing, the current interest rate for EE bonds issued Nov. 1, 2023 to April 30, 2024 is 2.70%.

While that’s not a very high interest rate, the main redeeming factor of EE bonds is that they will double your investment after 20 years, regardless of your fixed interest rate.

So if you purchase the maximum of $10,000 for an infant niece or nephew, they’ll have $20,000 waiting for them by the time they graduate from college. Best of all, they won’t have to pay any taxes on their withdrawal if they use it to offset their student loans.

Series I savings bonds

Series I savings bonds, or I bonds for short, have a variable interest rate that resets every six months to try and match the current rate of inflation.

At the time of this writing, the current interest rate for I bonds is 5.27% for bonds issued issued Nov. 1, 2023 to April 30, 2024.

More: Are I bonds a good investment?

Series EE vs. I bonds

Deciding which type of savings bond is best mostly depends on when you think the recipient might cash it in.

If it’s 20 or more years, Series EE bonds might be the better choice. At 20 years, your gift amount is guaranteed to double. That’s a solid rate of return for a savings bond, and historically speaking, will likely beat what they could’ve made from an I bond.

If it’s within 20 years, I bonds are the better gift. Simply put, the current interest rate for I bonds much higher than for EE bonds in the short-term. And even if rising interest rates finally curb inflation this year, the I bond rate will likely continue to beat EE rates on average for the next few years.

In the end, I think EE bonds are the perfect gift for infants and young children since they can use them to offset their student loans in their 20s. I bonds, meanwhile, are great for everyone else — especially during this period of high inflation.

Recipient info needed to buy savings bonds

To gift a savings bond, you’ll need to know the following information about the recipient:

- Full legal name

- SSN or other taxpayer ID

- *TreasuryDirect account number

Luckily, you can purchase savings bonds in their name and generate a physical gift certificate using just the first two.

*To transfer the bonds, you or their parents need to help them create a TreasuryDirect account.

How to buy savings bonds as a gift

TreasuryDirect has a quick reference guide on How to Buy a Gift Savings Bond, but here’s an expanded version with a few extra details and screenshots:

1. Create an account with TreasuryDirect.gov

TreasuryDirect is a mega-secure, government-hosted website for buying bonds directly from the U.S. Treasury. Be prepared to spend about 10 minutes creating an account. It’s all electronic and involves setting many passwords, security questions, etc.

One peculiar feature of TreasuryDirect is that it will not let your browser save your password. So definitely write that down somewhere, and help your gift recipient do the same in step 6.

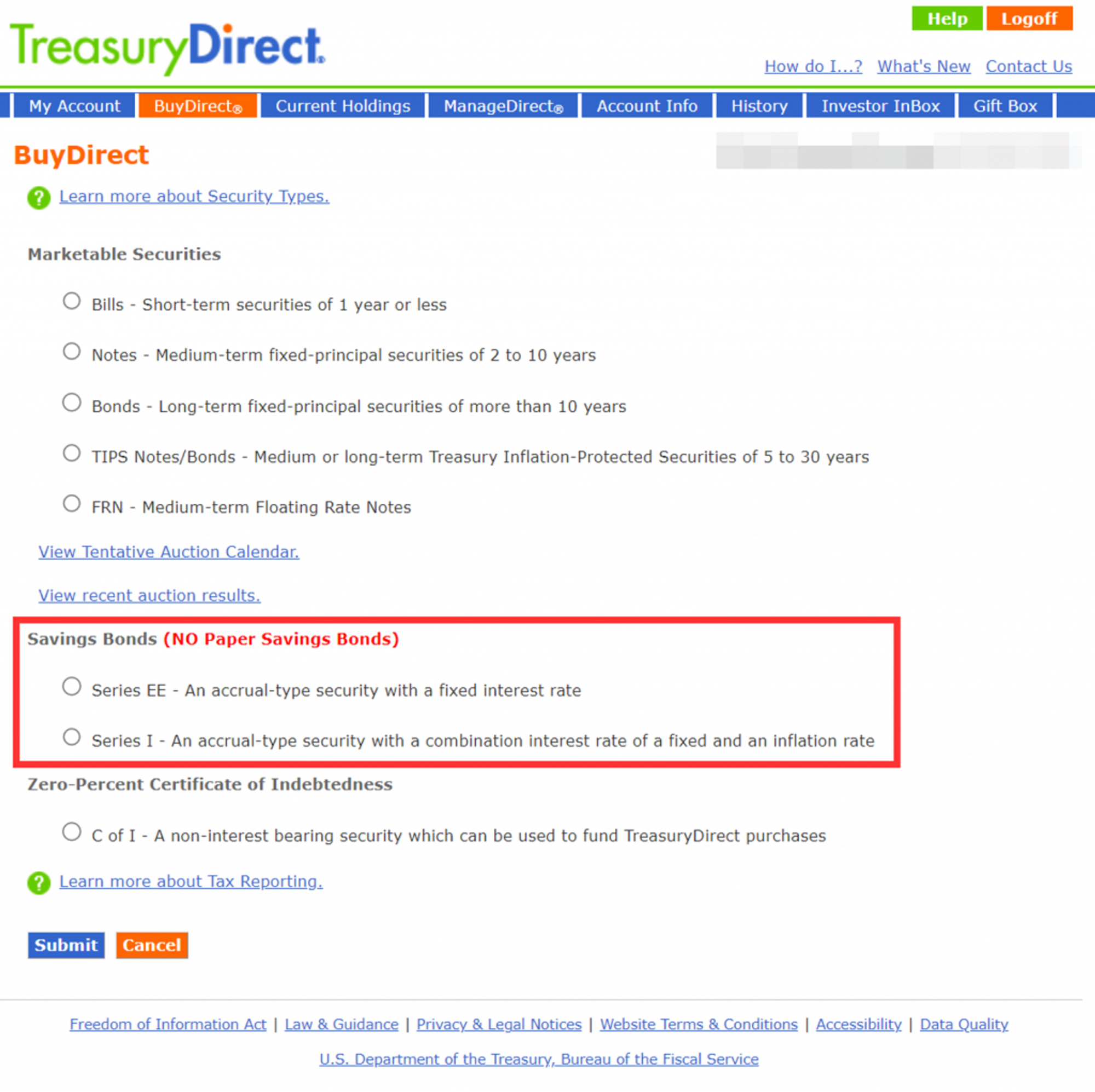

2. Visit BuyDirect and choose either EE or I savings bonds

Once you’re in, head to BuyDirect in your dashboard. There, you’ll see savings bonds halfway down. Check the box for either EE or I bonds and click “Submit.”

3. During checkout, add the recipient and check “This is a gift.”

Here, you’ll click Add New Registration, enter your recipient’s name and SSN, and check “This is a gift.”

4. Purchase the savings bonds

Once you purchase the savings bonds, you’ll receive a confirmation email, and the bonds will typically be added to your account within 24 hours. In my experience, they appeared by the morning of the next business day.

Do note, however, that your gift recipient has not received the bonds yet. They’ve been purchased and registered in their name, but they can’t access them without a TreasuryDirect account. We’ll create an account for them in Step 6.

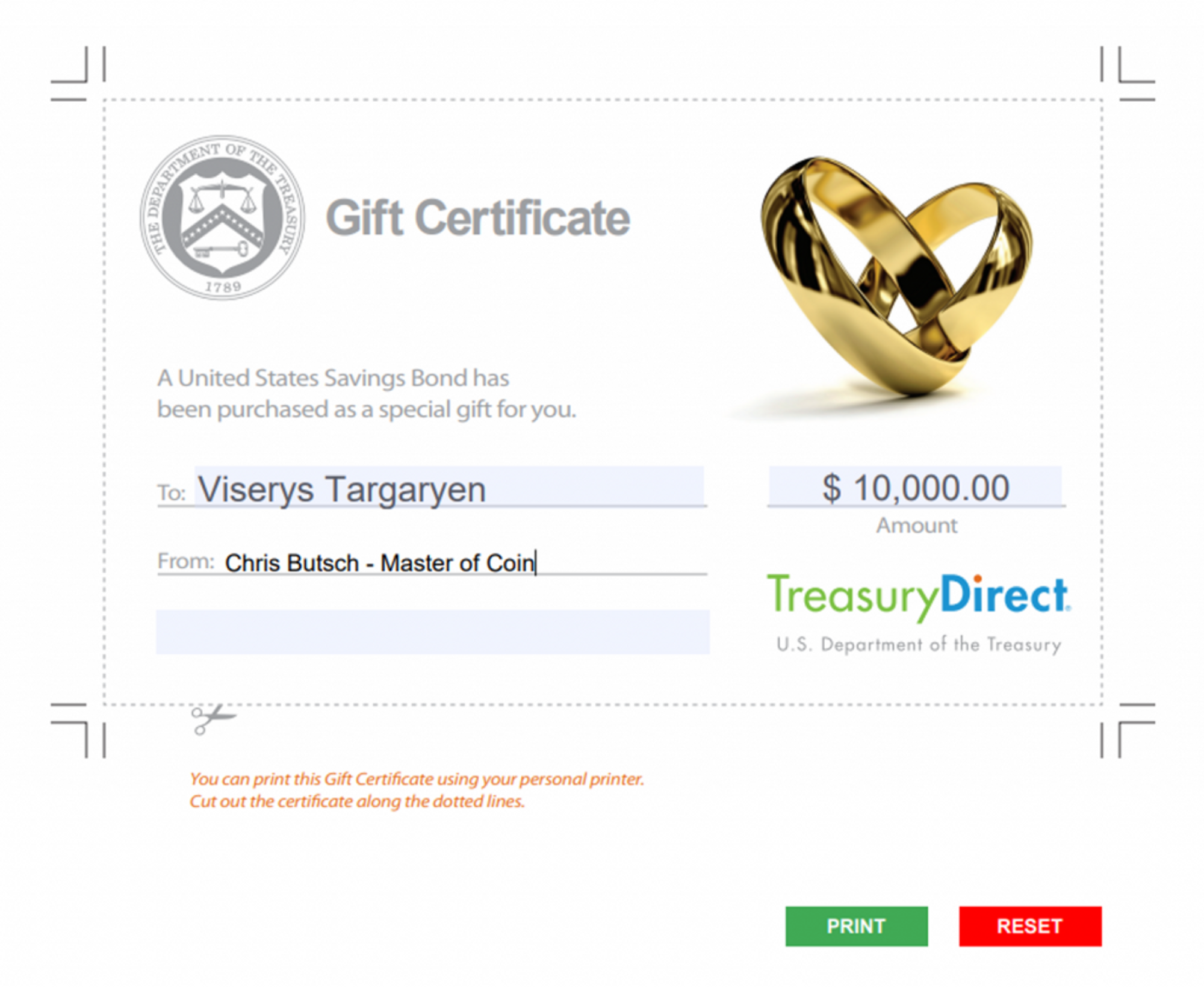

5. Print a gift certificate

The U.S. Treasury encourages you to print “one of our pretty gift announcements” to accompany your gift bond. They have 25 templates covering nine categories from “All Occasion” to “Baby” to “Graduation.”

You can access that page any time and print as many as you like; all of the information entered is 100% manual.

Once the recipient gets your thoughtful gift, your next step is to help them generate an account so they can officially take control of the bond.

6. Help the recipient generate a TreasuryDirect.gov account

In order to formally receive the bond, the recipient must generate a TreasuryDirect.gov account. Perhaps you can help them do it as part of the gift, or just have their parents do it.

Anyways, once they generate an account, get their Account Number from them and log back into your account.

7. Transfer the bonds from your gift box

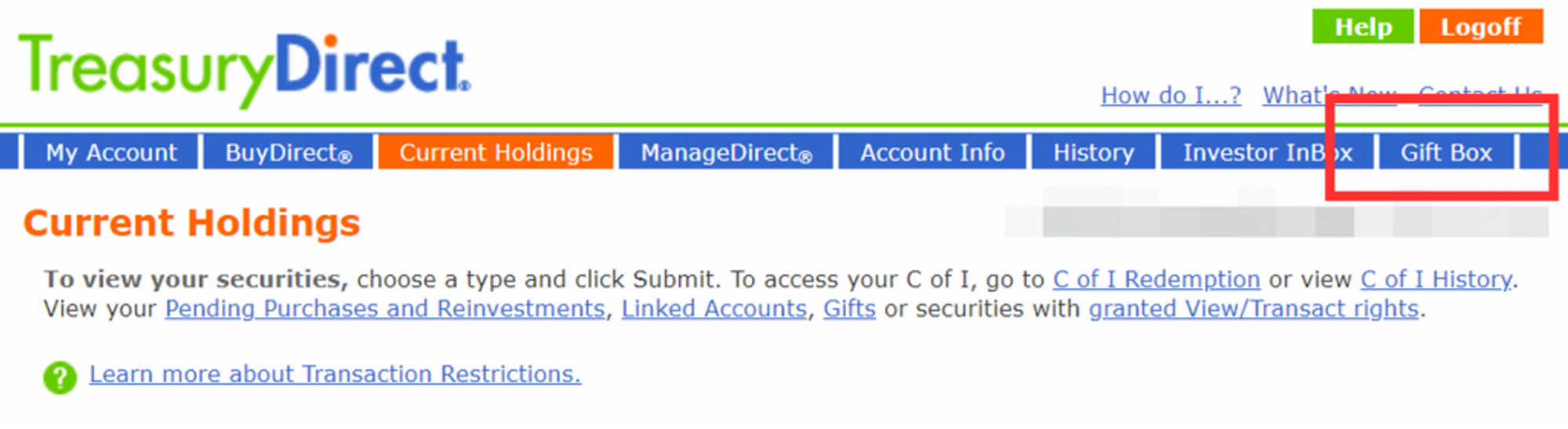

TreasuryDirect holds bonds you marked as gifts — but haven’t yet sent to anyone — in a particular area of your dashboard called your “Gift Box.”

This is where my screenshots end since I don’t have any gift bonds to send, but the remaining steps are pretty intuitive.

- Select the bond you wish to give.

- On the Detail page, click “Deliver.”

- Enter the recipient’s full TreasuryDirect account number on the Delivery Request page.

- On the Delivery Review page, if everything looks good, click “Submit.”

The transfer takes another business day.

Lastly, this may sound nuts, but you might even consider setting a calendar reminder for yourself — two, five, or 20 years in the future — to check in with your gift recipient. Unless they’re already well-organized with their finances, they may forget about their maturing bond.

Then, when you remind them at graduation that they have $20k waiting for them, it’s like getting credit twice for the same gift!

Tax implications of gifting savings bonds

When you give bonds as gifts, the recipient is responsible for paying taxes when they cash them in.

Thankfully, Treasury Savings Bonds aren’t subject to state or municipal taxes, ever. On the federal level, taxes may be waived if the recipient uses them to cover qualified higher education expenses (making them such a great future graduation gift).

The last thing to consider is interest reporting. Most people who cash in bonds only report their interest earnings during the fiscal year they cash them in. However, students who hold bonds might consider reporting their interest earnings sooner while they’re in a lower tax bracket.

The bottom line on savings bonds

In a way, savings bonds are the ideal gift; they’re unique, thoughtful, and valuable no matter who you buy them for. They may only illicit an “Oh, neat,” in the short term, but they can change the recipient’s life in the long term.

- Savings bonds make memorable and valuable gifts that could provide school loan relief or a rainy-day fund for the recipient.

- There are two types of savings bonds you can give as gifts: EE and I bonds. EE bonds are better if the recipient will cash them after 20 years; savings are better for less than 20 years.

- The purchasing and transferring process all happens through treasurydirect.gov.

You May Also Like

- JP Morgan sees gold hitting $6,000/oz before 2027 — and a Gold IRA lets you hold the physical metal while deferring the tax bill. Get your free guide from Priority Gold

- Dave Ramsey warns nearly 50% of Americans are making 1 big Social Security mistake — here’s what it is and the simple steps to fix it ASAP

- Thanks to Jeff Bezos, you can now become a landlord for as little as $100 — and no, you don't have to deal with tenants or fix freezers. Here's how

- Millionaires under 43 are reshaping investing — just 25% of their portfolios are in stocks. Here’s where their money is going

Chris helps young people prosper - both mentally and financially. In addition to publishing personal finance advice for Investor Junkie (now Moneywise) and Money Under 30, Chris speaks on the topics of positive psychology and leadership through CAMPUSPEAK and sits on the advisory board of the Blockchain Chamber of Commerce.

Investing • Jan 29

How to invest in cryptocurrency

Investing • Jan 02