Aug 31, 2020

Follow us on Google for more Moneywise news

Add us on Google

While we adhere to strict editorial guidelines, partners on this page may provide us earnings.

The thrill of hitting the road for the first time as a fully-licensed driver can be wrecked by steep car insurance costs.

New drivers are considered high-risk by insurers. Anyone who just got a license and has no driving record or insurance history can expect to face a higher premium than an experienced driver, and will even pay more than someone who's had insurance for only six months.

Advertisement

If you're just starting out behind the wheel and are shocked by the insurance rates you're being offered, here are a few tips for getting your policy at the best possible price.

Thanks for subscribing!

The insurance clarity you've been missing.

By signing up, you accept Moneywise Terms of Use, Subscription Agreement, and Privacy Policy.

Join an existing insurance plan

In the eyes of insurance companies, first-time drivers include not only teen drivers — who are notoriously expensive to insure — but also immigrant drivers who are new to U.S. roads, and adults who've just learned to drive.

We may see more Americans taking up driving at later ages if predictions are right that the coronavirus will lead remote workers to move to suburbs and rural areas from big, crowded cities. Some city dwellers have never learned to drive because they rely on mass transit.

The U.S. average annual car insurance premium in 2020 is $1,560, according to the auto insurance website The Zebra. What does a new driver pay, and how does that compare to rates for drivers at other experience levels?

- The premium for a first-time driver is around $1,730 per year.

- A driver with five years of continuous coverage pays 12.4% less, or roughly $1,515 annually.

- A driver with an insurance history going back just six months pays 7.2% less than the newbie, or about $1,605.

You could try lowering your cost by getting yourself added to a close family member's insurance plan — assuming your parent or spouse has a good insurance record.

But note that an insurance company often will raise the primary policyholder's rate for adding on a new driver. A teenager can boost a parent's auto premium by 50% or even 100%, says the industry group the Insurance Information Institute.

Must Read

- The ultra-rich use these 5 real estate strategies to build wealth while they sleep — you can start with just $100

- Here’s the average income of Americans by age in 2026. Are you keeping up or falling behind?

- Insurance companies profit most from drivers who auto-renew without shopping around. Comparing 100+ quotes takes 2 minutes and costs nothing

Join 250,000+ readers and get Moneywise’s best stories and exclusive interviews first — clear insights curated and delivered weekly. Subscribe now.

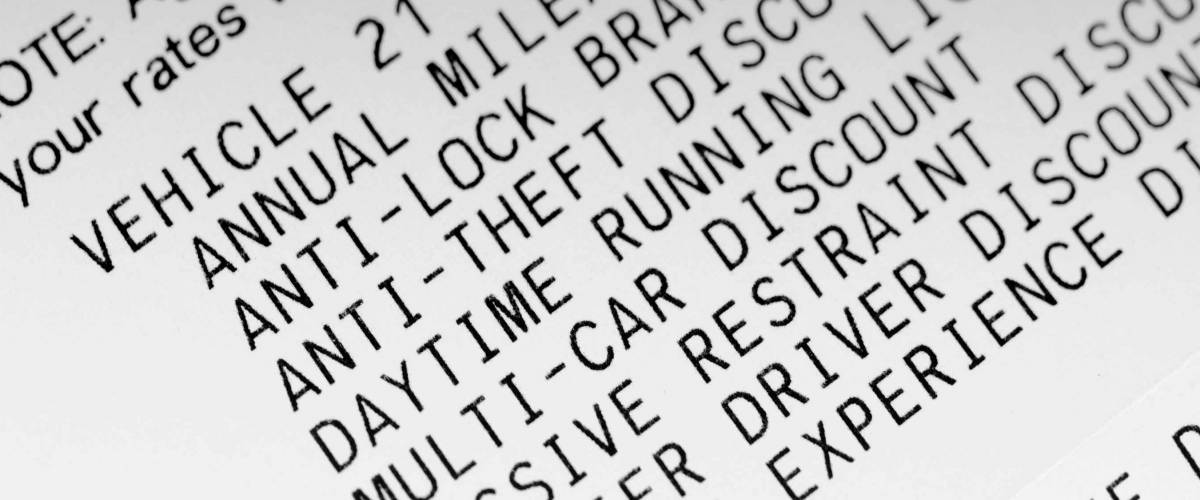

Look for discounts and other money savers

Car insurance policies typically come with a wide variety of available discounts.

Advertisement

Auto insurance is a very competitive business, and insurers use a slew of discounts to win new customers.

There are discounts for:

- Safe drivers with clean driving records.

- People who hold certain jobs, like schoolteachers and firefighters.

- Drivers whose cars are equipped with safety features including air bags, anti-lock brakes and even daytime running lights.

- Graduates of certain universities, or members of fraternities and sororities.

- Members of the military.

- Customers who agree to put a gadget inside their car that monitors their mileage and driving habits.

One of the most popular discounts is for "bundling" policies: buying your car insurance from the same company that provides your homeowners insurance or renters insurance. Liberty Mutual Insurance boasts that customers who bundle their auto and home insurance policies can save $842, while Progressive says buying multiple policies will save you an average 5%.

For new drivers who are students — in high school or college — common price breaks include:

- "Good student" discounts, typically for maintaining a B average or better.

- "Distant student" discounts, usually when a student spends a good part of the year away at a school more than 100 miles from home (and the family cars).

Other money savers technically aren't discounts but involve the way you structure your policy. For example, you can cut some coverage costs by up to 40% if you raise your deductibles — your potential out-of-pocket costs following an accident — from $200 to $1,000, the Insurance Information Institute says.

Shop around regularly

Advertisement

You’re not locked into the same car insurance policy for life, so don’t overpay when you don’t need to.

When you're a brand-new driver who's paying steep insurance premiums, you should expect to see those costs come down fairly quickly if you maintain a clean driving record and don't file any claims. As we said earlier, a first-time driver typically saves more than 7% after only six months of continuous insurance coverage.

Policies often renew every six months, and each time you get your notice that it's time to pay again you need to shop around and check rates from multiple insurance companies — to keep making sure you're getting the best deal.

Though some insurance companies offer modest "loyalty discounts" to longtime customers, insurers can be just as likely to raise your rates if you stay put and seem unlikely to bolt. The Consumer Federation of America says this practice is called "price optimization."

Annual policies are less common than those with six-month terms. If your car insurance renews just once per year, you might still make a switch before the term is up — as long as your insurance company doesn't charge a cancellation fee. Not all insurers have one of those, so check your policy.

Whenever you're rate shopping, be sure to let your current insurer know you’re scoping out the competition. If you find that another company will offer you a lower rate, your current insurer might be willing to match the price. It's a way to stick with an insurance company you might like, and get a good price break for keeping your business there.

You May Also Like

- JP Morgan sees gold hitting $6,000/oz before 2027 — and a Gold IRA lets you hold the physical metal while deferring the tax bill. Get your free guide from Priority Gold

- Dave Ramsey warns nearly 50% of Americans are making 1 big Social Security mistake — here’s what it is and the simple steps to fix it ASAP

- Thanks to Jeff Bezos, you can now become a landlord for as little as $100 — and no, you don't have to deal with tenants or fix freezers. Here's how

- Millionaires under 43 are reshaping investing — just 25% of their portfolios are in stocks. Here’s where their money is going

Serah Louis is a reporter with Moneywise.com. She enjoys tackling topical personal finance issues for young people and women and covering the latest in financial news.